Russian Oil Production

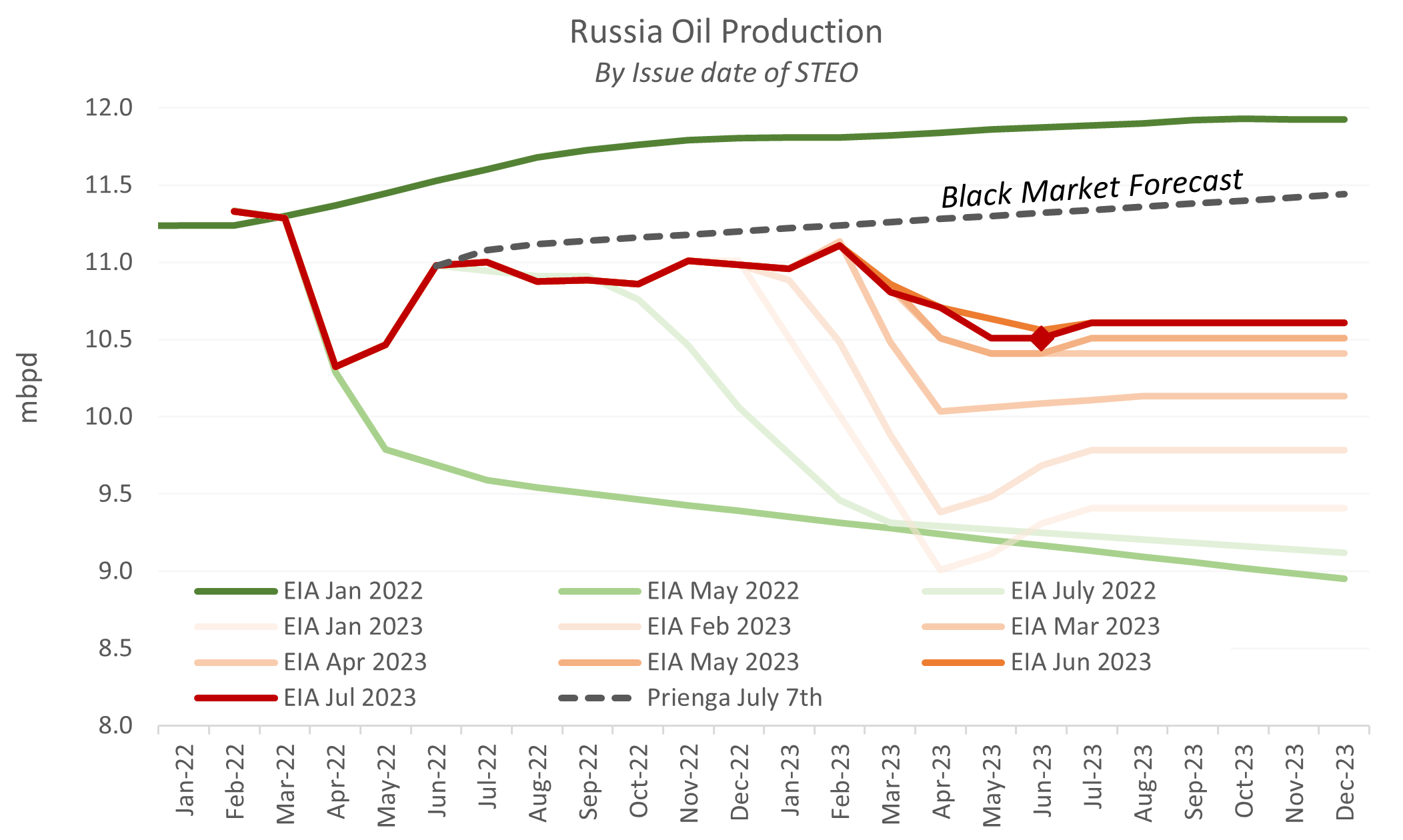

The EIA issued its estimates for Russian oil production this past week. The EIA is the statistics arm of the US Department of Energy. It issues a large number of reports, including its monthly Short Term Energy Outlook, which is one of the wonders of the analytical world and the source of data on the graph below.

The EIA reports that Russian oil production fell to 10.5 mbpd in June, a bit below earlier estimates and 7% below its pre-war level. This is also 11% below EIA's pre-war forecast for Russian oil output, which in fact is similar to observed reductions in other prohibitions. For example, in the Prohibition of the 1920s, per capita US alcohol consumption fell by 15%. Prohibitions, including price caps and embargoes, are almost universally unsuccessful, a theme to which I regularly return in these analyses. For now, the EIA sees Russia's June oil production as the low point going forward. I think it fair to say that the EIA has low confidence in its forecast, but in any event, it anticipates no further reductions in Russian oil output.

Russian Crude Oil Prices

Russian crude oil prices are generally linked to its Urals oil price to the west and the ESPO (Eastern Siberia–Pacific Ocean oil pipeline) price to the east. Historically, both the Urals and ESPO prices were essentially indistinguishable from the European benchmark Brent oil price, at most with a discount of $1-2 / barrel. Since the start of the war, however, the Urals and ESPO prices have diverged from Brent by as much as $35 / barrel.

A price cap of $60 / barrel was implemented by Ukraine's western allies on December 5th. Since that time, the Urals price has generally remained below the cap threshold. By contrast, the ESPO price has never fallen to or below the cap level.

The last reported price for Urals was $60.06 / barrel, that is, above the cap level. This is not the first time this has occurred, as the posted Urals price was above the cap for most of April.

Russian Oil Price Discounts

Russian oil prices can also be viewed in relation to Brent. The Urals discount -- the difference between the Urals and Brent oil prices -- now stands at just under $20 / barrel, where it has been since mid-April. Note that the Urals discount is effectively the smallest since the start of the war and smaller than before the imposition of either the embargo or price cap. This is similarly true for the ESPO discount (the difference between the ESPO and Brent oil prices).

This suggests that the discount, rather than the price cap, is gating the Urals oil price. That is, if Brent rises, the Urals price will follow at a distance of $20 / barrel. Brent is just above $80, and the Urals is just above $60. If Brent moves to $90, then Urals may be plausibly expected to rise to $70.

Of course, the western allies can move to sanction Greek shippers and Indian oil refineries for price cap breaches, but this comes at a political cost. Further, the higher the Brent oil price, the less political leverage the western powers will enjoy.

Forecasting oil prices is a hazardous occupation, but oil demand is expected to outstrip supply for the balance of the year and into 2024. Higher Brent prices are certainly possible.

Urals today stands at $60 and ESPO above $71, implying an aggregate selling price around $63 / barrel for Russian crude oil exports. The Urals and ESPO oil prices averaged $56 / barrel from 2015 to 2021. Current Russian selling prices are therefore already above the prior seven years' average. If Brent moved up to, say, $100 / barrel, Russia's finances could improve quickly and materially.

The price cap and embargo as currently implemented are misspecified and counter-productive. Chinese and Indian interests are capturing the value of the Urals oil price discount, which in turn serves as 'store credits' for Russia to purchase influence and physical goods. Put another way, the price cap is channeling funds into the Chinese military industrial complex when, were the cap properly structured, those funds would go in significant part to the US defense industry. We are speaking of billions of dollars.